How Park Wealth Management Can Help You Save More For Retirement:

Case Study – High Income Individual Business Owner wants to make large retirement plan contributions – married with no employees:

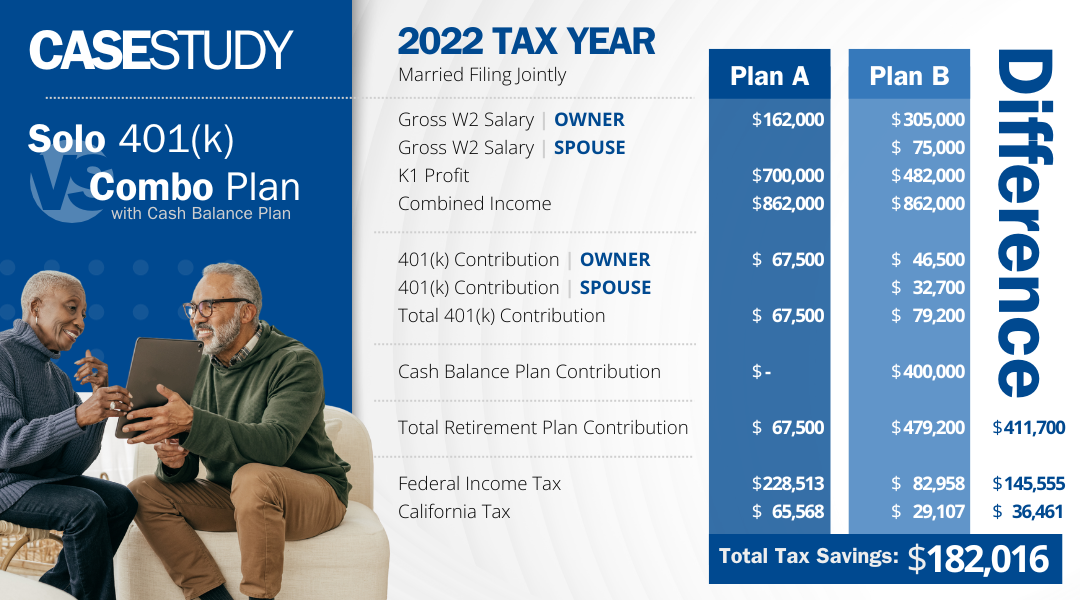

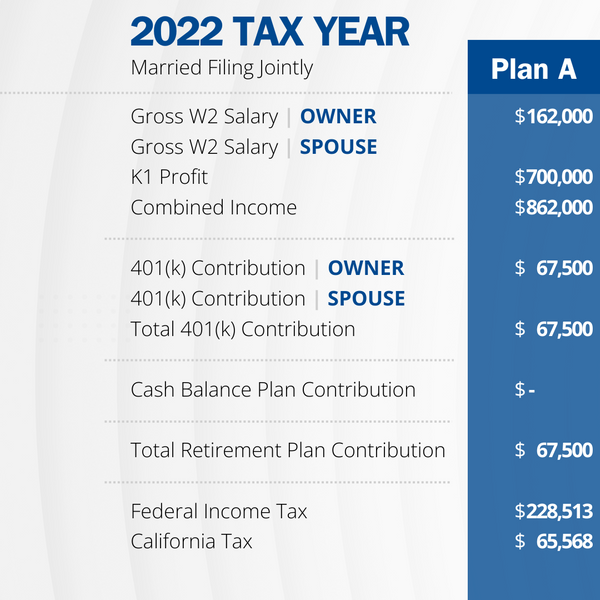

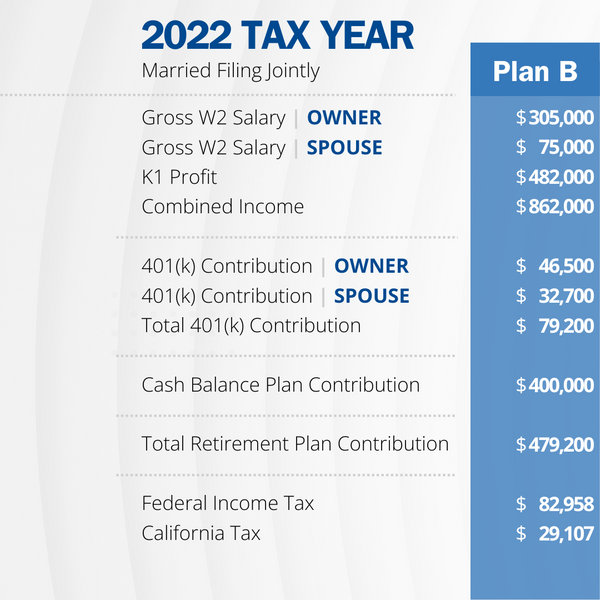

This analysis will compare (2) scenarios where the business owner of an S Corporation would like to increase their retirement plan contribution in 2022. With a custom combo plan, we can increase tax-deductible retirement plan contributions from $67,500 to $479,200 and increase the Federal & State tax savings by $182,016. Instead of paying the government $182,016, you save this money for retirement and in nearly every instance are taxed at a much lower rate when you do use the funds.

We are here to help you navigate the intricacies of retirement plans. Schedule an appointment with a financial advisor to get a plan custom to your unique goals.

Plan A – Solo 401(k):

A 63 year old business owner takes a large enough W2 compensation to make the maximum allowable contribution into a Solo 401(k) Plan. This contribution is made up of (3) Components:

1) Salary Deferral – This must be deducted from the employee’s paycheck and contributed into the account within 7 business days. The maximum contribution is $20,500 for 2022.

2) Catch Up Contribution – This must also be deducted from the employee’s paycheck and contributed into the account within 7 business days. The maximum contribution is $6,500 for 2022.

3) Profit Sharing Contribution – This contribution is due at the Corporate Tax Filing Deadline of March 15th or if filing an extension, September 15th of the following year and prior to the corporate tax returns being filed. The maximum is 25% x W2 Compensation up to $305,000 for 2022.

Plan B – Solo 401(k) plus Cash Balance Plan:

The business owner increases his W2 Compensation to the maximum Annual Compensation limit of $305,000 in 2022 and begins paying his spouse $75,000 compensation for employment.

Both the business owner and their spouse participate in the 401(k) Plan and Cash Balance Plan leading to larger allowable contributions. The Cash Balance Plan Contribution is based on their age and Compensation.

If the business slows down and the owner would like to decrease contributions, the 401(k) Contributions are all discretionary and we could reduce the W2 Compensation. This would decrease the required Cash Balance Plan contributions and provide flexibility to the owner. Since there are (2) retirement plans, the 401(k) Contributions are reduced.

Compare the Difference

Download the full PDF to save for your reference. In this particular case, this client was able to save over $182,000!